RETIREMENT

Reality Check

Most financial advisors recommend saving at least 10 percent of your gross salary each paycheck. The Social Security Administration recommends setting aside 15 percent or more for retirement savings. To capture the full benefit being offered by your employer, you should, at a minimum, contribute enough to your 401(K) to collect all matching dollars being offered.

The old rule of thumb used to suggest you subtract your age from 100, and that's the percentage of your portfolio that should be kept in stocks. (For example, if you're 30, 70% of your portfolio should be in stocks. If you're 70, 30% of your portfolio in stocks.)

However, with Americans living longer, many financial planners are now recommending that the rule should be closer to 110 or 120 minus your age. (For example, if you're 40, 70-80% of your portfolio should be in stocks.) The new thought allows you more time to take advantage of the extra growth stocks can provide. (Source: CNN MONEY)

AARP finds that 55-million private sector employees in the United States have no access to retirement savings plans at work. In addition, those who freelance or are self-employed also do not have employer offered retirement savings plans.

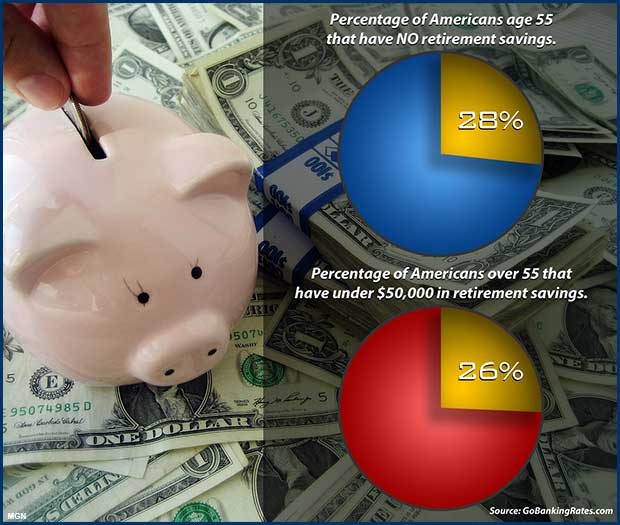

The Center for Retirement Research analysis finds that about half of American households will be unable to maintain their standard of living in retirement. To avoid having less income in retirement, households should be saving more prior to retirement—more so than past generations.

There are several reasons today’s retirees are not able to maintain their standard of living in retirement. Many current retirees do not have the luxury of a pension account from their employer. In 1979, 28 percent of all private-sector workers had pensions as their sole retirement plan benefit; by 2011, that number had dropped to 3 percent, according to the Employee Benefit Research Institute. Back in the early 1980s, double-digit interest rates meant that it was possible for many retirees to live comfortably off of bond income.

Review the full MarketWatch report on Standard of Living in Retirement.

STATE SPONSORED RETIREMENT INVESTMENT PLANS

AARP spent the Spring of 2017 attending the Joint Finance Committee Hearings around the state as it heard from the public on the upcoming state budget. AARP is endorsing a state sponsored retirement plan that was first introduced back in 2015 under Wisconsin Senate Bill 45.

The 2015 legislation aimed to establish a private retirement security plan to provide retirement benefits for residents of the state who choose to participate in the plan. It would not replace employer retirement plans. The plan failed to pass at the time, but the measure is expected to be brought up again this year either as part of the budget or later as a stand-alone bill, according to AARP Wisconsin.

TRUMP ADMINISTRATION CHANGES TO OBAMA ADMINISTRATION RULE

Congress took the first step in February 2017 to roll back an Obama-era rule that paved the way for state sponsored retirement investment plans. Resolutions to block Department of Labor rules allowing states to set up private-sector retirement savings programs were introduced by members of the House Education and the Workforce Committee.

Plans previously approved by California, Connecticut, Illinois, Maryland, New Jersey, Oregon, and Washington could all be in jeopardy before they are implemented. Several other states have considered such plans, including Wisconsin in 2015.

Wisconsin Senate Bill 45 introduced during the 2015-16 Legislature aimed to establish a private retirement security plan to provide retirement benefits for residents of the state who choose to participate in the plan. The plan failed to pass.

RAISING SOCIAL SECURITY FULL BENEFITS AGE

The retirement age of 65 to collect full social security benefits is no longer the norm. A law passed in 1983 has slowly been raising the age in which retirees can collect full retirement benefits provided through the federally funded Social Security Administration.

Those retiring in 2017 would receive 100 percent of Social Security benefits at age 66. Those born after 1960, the full Social Security benefit retirement age would be 67.

The earliest a person can start receiving partial Social Security retirement benefits is age 62, when you will get 75% of the monthly benefit.

In 2016, The Social Security Reform Act of 2016 was introduced that would gradually raise the full retirement age at which workers can claim benefits. It would raise the age to 69 for those who qualify for "early retirement age" after Dec. 31, 2029.

LINKS TO REVIEW ABOUT RETIREMENT